Frequently Asked Questions

TERS FAQs – December 2020

The following FAQs have been created based on information found in the UIF's 15 and 18 December TERS update letters. They are purely for informational purposes. If you have any further questions off the back of the FAQs, please contact the UIF on 0800 212 799.

I'm waiting for my application to be processed; when will this be completed?¶

The UIF re-ran all pending applications for the lockdown TERS periods over the weekend of 19 December, meaning that your application may have been processed then.

If it has not been, the UIF is now processing TERS periods on a weekly cycle to pick up the applications which have been corrected. Your applications will only be processed once any error message present has been resolved. The weekly schedule is:

| Day | Period |

|---|---|

| Monday | 27 March to 30 April and 1 to 31 May 2020 |

| Tuesday | 1 to 30 June 2020 |

| Wednesday | 1 July to 15 August 2020 |

| Thursday | 16 August to 15 September 2020 |

| Friday | 16 September to 15 October 2020 |

| Saturday | Discrepancies for all periods |

The CSV that I used resulted in no employees appearing on the TERS portal. What can I do?¶

The CSV that SimplePay generates for you has been extremely successful in aiding our clients with their applications and we haven't heard of such issues. Therefore, if you are new to SimplePay, why not give our automatically generated CSV a go?

However, if you have experienced this issue whilst using the SimplePay CSV, please get in touch with us so that we can assist you with completing the submission.

What are discrepancies in relation to my application and how might they be caused?¶

Discrepancies are occurrences where your employee has received less TERS benefits amounts than they are entitled to. This can often be the result of the information which informs the amount of benefits your employees receive being incorrectly submitted. Instead of resubmitting, there is a discrepancy process you can follow to confirm your employee gets the correct amount.

Discrepancies for the 16 August to 15 September and 16 September to 15 October application periods have been added to the Discrepancies tab in the TERS portal. You can make amendments on the TERS portal throughout the festive period, but any amendments you make will likely only be processed in the new year.

You can read more about discrepancies and what may cause them in this UIF letter from 10 August 2020.

I have an error that says something about integration with the TERS financial system. What does it mean?¶

While doing some recent updates to the TERS platform, the UIF introduced two new validation messages:

- "TERS Vendor integration could not be done with financial system", which can result from: * Your Vendor ID having a discrepancy for one of the payment cycles. Once TERS financial reconciliation is complete, the ID will be processed. * Your bank details have been verified, but manually, meaning that your payment will be done separately to the automatic process. * The employee in question is a foreigner and so will be paid separately to the automated process.

- "TERS Payment integration could not be done with financial system", can be as a result of an ID failing bank verification, or being down as someone who's recorded as deceased.

Neither error message requires any action on your part at this stage. They should be resolved in the reconciliation process, after which your claim should be processed, or a more specific error descriptor will appear.

How can I get each individual employee's refund amount recorded on the TERS system?¶

Developments to the online portal now allow you to view the refunds you've made to the UIF. However, if for any reason you need to record the amount refunded per employee, you need to complete a template spreadsheet with the relevant information and return this to the UIF.

You should have received the template, instructions on how to submit the amounts refunded per employee and the update letter from the UIF by email on 19 December 2020. If you did not receive the email, but need to complete this process, please contact the UIF for assistance on 0800 212 799.

When will the UIF be closing for the festive period?¶

Members of the UIF have delayed the date of their normal festive break to continue processing TERS payments. The UIF will now close on 24 December 2020 and reopen on 4 January 2021. You can however continue to update information on the TERS portal throughout this period.

Why is my employee's tax lower than expected after lockdown?

With employees returning to work and earning an income again, we have noted that the impact of lockdown is still present. The most obvious impact to the first payslip that is processed, is the lack of or reduced amount of PAYE. We would like to reassure you that it is expected due to the months that the employees have earned no income or greatly reduced income during lockdown.

SimplePay uses the Annual Equivalent calculation method that SARS uses to calculate the employee's PAYE. This calculation divides the year to date income by the number of periods employed during the tax year to determine the average income, which is annualised to determine the PAYE. With the lockdown months of no/reduced income, the average income that is annualised is much lower – the periods employed have not decreased but their income per period has. This results in a lower year-to-date tax liability so when the year-to-date tax paid is subtracted, the liability for the period is very low or 0.

Note that this is only the case if the employee was terminated on a long-term absence code (9, 10, 17, 18 and 19 – code 17 being most common in lockdown) or if you've left them active but processed 0 payslips for the lockdown period. If the employee's service was ended using any other code besides the aforementioned and you are concerned about the tax calculation, please get in touch if the below resources don't help.

You can view the details of a particular employee's Tax calculation via the Tax trace link on the Payroll screen. Please also see our help page on Employees' Tax for a detailed explanation of the Annual Equivalent calculation.

Why are the UIF and SDL amounts on the payslip different?

Generally, if an employee has a very simple payslip, with only a basic salary for example, the UIF and SDL amounts will be the same. However, there are certain circumstances in which these amounts will differ – this is because UIF is calculated on an amount known as remuneration for UIF purposes while SDL is calculated on remuneration for SDL purposes.

- Remuneration for UIF purposes is the employee's total remuneration, less any exclusions. The most notable exclusion from UIF is commission.

- Remuneration for SDL purposes is generally the same as remuneration for PAYE purposes, namely the employee's total remuneration less any taxable income deductions, such as from retirement funds. Sometimes, however, additional SDL exclusions will apply.

The two most common reasons for a difference in UIF and SDL are, therefore, that the employee:

- Earns commission, which is UIF exempt, as well as their basic salary / hourly pay; and/or

- Has a retirement – pension / provident / retirement annuity – fund, which gives rise to a taxable income deduction.

You can view what income is included in the UIF calculation and SDL calculation by viewing the UIF trace and SDL trace respectively.

More information on all of the above concepts, as well as the UIF and SDL trace, can be found on the following help pages:

What relief measures are there for employees?

The Government has announced several relief schemes and initiatives in an attempt to support South African businesses through the Lockdown period. As a minimum, all businesses impacted financially by the COVID-19 pandemic should apply for TERS for their employees.

In addition to TERS and the other initiatives in place to assist businesses to pay employees (outlined in the question below), individuals can also apply for Social Relief of Distress grants.

What relief measures are there for businesses?

The Government has announced several relief schemes and initiatives in an attempt to support South African businesses through the Lockdown period. In a nutshell, the following options exist at the time of writing:

- Expansion of the Employment Tax Incentive (ETI)

- The COVID-19 Temporary Employer-Employee Relief Scheme (TERS)

-

Deferred tax liabilities for certain businesses on which SARS has published a Disaster Management Tax Relief FAQs document

- Contents of note within this document are:

- An outline of the requirements to be able to claim employee's tax relief

- An outline of the expansions made to the Employment Tax Incentive (ETI)

- A worked example of how the employees' 35% tax deferral will work

- An SDL payment holiday from 1 May to 31 August 2020

Provisional tax deferral

There is also information on provisional tax deferral in this document. We regret to inform you that this is beyond our scope of services and so we are not able to assist with this scheme.

- Contents of note within this document are:

- Various financial support and relief measures for SMMEs, including:

- Debt Relief Finance Scheme; and

- Business Growth and Resilience Facility.

My business is closing temporarily during lockdown, what UIF code should I use?

It is possible to claim UIF for employees for temporary closure of your business, however this requires that each employee has an individual application completed.

To the best of our knowledge and based on advice we've received, it seems that wherever possible, employers are encouraged to apply for TERS rather than having employees go through UIF. The employer or the UIF will then distribute the allowance to their employees.

This will effectively allow for consolidated claims rather than many thousands of claims from individual employees, which will hopefully reduce strain on the UIF and allow for some measure of effectiveness in paying out benefits.

For any queries more detailed than this, we still recommend contacting the UIF or TERS phone lines.

You can find a handy overview of the forms and contact details required for the various UIF claims in our COVID-19 UIF Quick Reference Guide.

What support can my employees receive if they contract COVID-19 at work?

Should one or more of your workers contract COVID-19 at work, they can apply to the Compensation Fund, under COIDA. Support can include a:

- pay-out for temporary disablement while the worker is in quarantine, self-isolation or hospitalized;

- payment of medical expenses; and

- where, tragically, the illness results in fatality the Fund will pay out survivor benefits to dependents in the form of a monthly pension and funeral benefit.

Details on how to apply for the above compensation can be found in this Government Notice.

My employees will be working reduced hours and need to claim UIF, which code do I use?

Wherever possible, employers are encouraged to apply for TERS rather than having employees claim UIF. The employer or the UIF will then distribute the allowance to their employees.

As the TERS scheme has no effect on the employee's UIF credits, it is advisable that, if applicable, the TERS system is utilised up to its conclusion.

What is the 35% PAYE deferment?

Employee income, other than as a result of a TERS or UIF payout, is subject to PAYE at the usual tax rates.

Employers are responsible for withholding the PAYE from employees and paying this over to SARS. SARS has allowed for a deferred payment of 35% of employees' PAYE for the periods 1 April – 31 July. In other words, you can deduct the PAYE from employee's payslips, but only pay over 65% of the PAYE owed to SARS immediately. The remaining 35% can then be paid after the 31 July.

Repayments shall be spread equally across the six months following the deferment period.

SARS has confirmed that the PAYE reported on the EMP501 is the total PAYE liability and not only the PAYE due (PAYE liability less deferred amounts). The actual amounts paid for the relevant months should be completed in the Payment column on the EMP501. If the PAYE deferral was utilised, it will mean that a shortfall has been paid and the EMP501 will force a reason for which you have to complete "PAYE DEFERRAL".

I have employees who are ill as a result of COVID-19 and need to claim UIF, which code should I use?

Employees who are ill due to COVID-19 are entitled to claim a special illness benefit through the UIF. When ending their service, please use code 10.

For details on ending an employee's service on SimplePay, see the Ending an Employee's Service help page. Remember to also capture the anticipated reinstatement date at the same time so that we can generate a complete individual UI 19 for each employee.

What ETI changes are there for COVID-19?

We have provided a detailed help page on ETI for COVID-19 here.

How do I get the SDL payment holiday?

It has been reiterated that no contributions towards the SDL are necessary for the months of May to August. As it is a suspension, this means that you will not have to pay these months' contributions at a later date.

We have made the necessary amendments so that these changes are reflected in EMP201 submissions for the relevant periods.

My business is having to close down completely and will not reopen after lockdown. Which UIF code should I use for my employees?

In cases where your business unfortunately has to cease trading entirely and will not reopen after lockdown, you should use code 14 when ending employees' service.

For details on ending an employee's service on SimplePay, please see our help site.

More information on UIF codes is available in our COVID-19 UIF Quick Reference Guide.

I am an employee, will I be able to claim TERS / UIF because of COVID-19?

Employees can apply for TERS or UIF if their employer or Bargaining Council are not able to assist. However, as we simply provide software to employers, we are unfortunately not able to assist employees with their claims. Please contact your employer directly for any queries in this regard.

Is TERS the same as UIF?

Although TERS is administered by the UIF Commission, TERS benefits and UIF benefits are distinctly different. Each have their own eligibility requirements and the calculation of the benefits under each differ.

- UIF benefits are for those individuals who are unemployed or who are temporarily unable to work for reasons other than the impact of the COVID-19 lockdown (e.g. maternity leave, dismissal for poor performance, long-term illness)

- TERS benefits are for those individuals who are temporarily unable to work or who are unable to work at normal capacity due to the COVID-19 lockdown period. TERS provides relief for those whose income has been impacted by COVID-19.

Can an individual claim both?¶

Individuals cannot claim both UIF and TERS benefits. Therefore, if an individual has applied for UIF benefits for maternity leave, they should not be included in the employer's TERS application.

Should we apply for TERS or UIF?¶

The UIF Commission has indicated that employees who are retrenched or on reduced working time should receive TERS benefits rather than UIF benefits until further notice. This is to lessen the administrative strain on the UIF, as TERS requires applications to be submitted by employers on behalf of all qualifying employees, whereas UIF relies on individual UIF applications from employees.

Does TERS impact UIF benefits?¶

Claiming TERS has no impact on UIF credits. Any UIF benefits that you may be entitled to are unaffected by the receipt of TERS benefits.

How do I apply for TERS?

The COVID 19 TERS online applications section on the website of the Department of Employment and Labour seems to have been closed.

If you have an outstanding or unresolved TERS query, you can still try contacting the UIF call centre on 0800 030 007. However, new applications for COVID-19 TERS benefits are no longer being accepted.

The Department of Labour has stated that I, the employer, can complete the application on my employee's behalf. How do I do this?

Once all the relevant documents have been completed for the employee, rather than transferring them to the employee, you must email all the required documents to the nearest UIF Processing centre to you.

SimplePay assists with the completion of the individual UI-19 and UI-2.7 forms. For more information on these, see the Ending an Employee's Service help page.

How can I track the progress of my TERS application?

The tracking tool on labour.gov.za seems to have been removed.

If you are still dealing with this, you can try calling the TERS hotline on 0800 030 007.

Who do I contact for assistance with UIF and/or TERS?

There are a few different options for contacting the relevant people at the Department of Labour:

- Dedicated TERS Hotline: 0800 030 007 and 012 337 1997

- UIF Call Centre: 0800 UIF (0800 843 843)

- UIF Provincial Rapid Response teams (for businesses with 50 employees or fewer)

- Eastern Cape – Manager: Philiswa Madikazi; Tel: 043 701 3342

- Free State – Manager: Morgan Ramatsetse; Tel: 051 505 6362 / 6200

- Gauteng – Manager: Dingaan Basimane; Tel: 011 853 0303

- KwaZulu-Natal – Manager: Gugu Khomo; Tel: 031 366 2012

- Limpopo – Manager: Ronet Landman 015; Tel: 290 1703

- Mpumalanga – Manager: Evelyn Mokoena; Tel: 013 655 8742

- Northern Cape – Manager: Adv Bulelani Gwabeni; Tel: 053 838 1554

- North West – Manager: Selete Qhamakhoane; Tel: 018 387 8178

- Western Cape – Manager: Tony Lamati; Tel: 021 441 8054

- UIF Email and fax to email numbers

- [email protected]; 0864397295

- [email protected]; 0864397296

- [email protected]; 0864397299

- [email protected]; 0864397300

- [email protected]; 0864397301

- [email protected]; 0864397302

- [email protected]; 0864397303

- [email protected]; 0864397304

- [email protected]; 0864397305

- [email protected]; 0864397306

- [email protected]; 0864397297

- [email protected]; 0864397298

- [email protected]; 0864397309

- [email protected]; 0864397294

- [email protected]; 0864397290

How long does TERS run for and what are the application deadlines?

On 21 July the Deputy Minister of Employment and Labour announced an extension of the TERS scheme by an additional one and a half months, to 15 August 2020.

Additionally it was proposed that applications for April, May and June TERS benefits will be closed at the end of July. This will not affect valid applications that have already been received by this date.

When do TERS applications close?

The proposed deadline date for April, May and June applications is 31 July 2020.

Part of the TERS application is proof of income for the employees – how do I provide this from SimplePay?

From our understanding of the requirements, proof of payroll is required and three months' payslips should be sufficient here. You can download all of your employees' payslips for a particular month (or pay period) from the Pay Runs tab in SimplePay. Please take a look at this help page for more information.

If you would like to see this information in report form, you can download our Transaction History Report. This is likely not sufficient to qualify as proof of income but may be useful for your own checks and records. More information on using our reports can be found on the Reports help page.

[Archive] Is TERS available for May 2020?

Applications for May TERS opened on 28 May 2020.

However, new applications for COVID-19 TERS benefits are no longer being accepted.

Does employee income still attract PAYE during the COVID-19 period?

Employee income, other than as a result of a TERS or UIF payout, is still subject to PAYE at the usual tax rates.

Employers are responsible for withholding the PAYE from employees and paying this over to SARS. SARS has allowed for a deferred payment of 35% of employees' PAYE for the periods 1 April – 31 July. Repayments shall be spread equally across the six months following the deferment period.

[Archive] I applied for TERS for April and May, but my employee only received a pay out for May. What do I do?

The UIF has advised that the employer does not need to do anything. The UIF system will do a "re-rerun" and will make payment for April. The UIF system does a re-run every three to four days.

I am registered with SARS for UIF, but not with the Department of Labour. Can I receive TERS benefits?

Many employers are registered with SARS for UIF payment purposes, but have never signed up with the UIF. As TERS benefit claims require a UI Registration number, some employers have been unable to apply for TERS benefits. SARS is now assisting the UIF with registering all SARS-registered employers with the UIF.

Once this is completed, the newly registered employer can submit back-dated declarations as far as possible, facilitating them in claiming the TERS benefit.

[Archive] Can I still apply for TERS benefits in May if I didn't apply in April?

An issue arose for employers wanting to apply for the first time in May. As they had not received any previous disbursements, they could not attach proof that they had disbursed the money to their employees.

The UIF advised that employers should substitute in a letter stating that they did not apply for March / April TERS benefits. The letter should ideally have the following characteristics:

- Letter has the company letterhead

- Signed by the director / head of the company

- Must be in PDF format

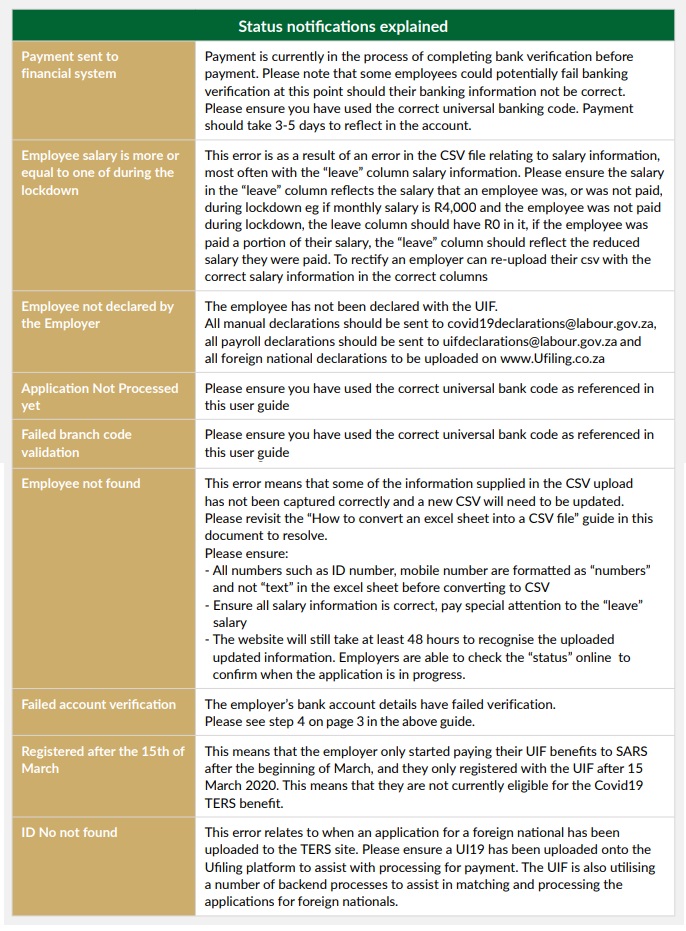

I've received feedback on my TERS application – what does it mean?

How should I reflect TERS advances on my EMP201?

If financially able, you can advance TERS benefits to your employees in the interim between application and disbursement of funds, recouping the money you have advanced from the TERS benefits paid into your account.

Here are some general points which you should consider when deciding how to reflect an advancement:

- If you, the employer, haven't received TERS benefits yet, and want to confirm that you do not advance more money than the value of the TERS benefit (as this shall be deemed a non-reclaimable top up), you should advance R 3,500 as this is the minimum amount an employee will be granted by the UIF under TERS. You can pay the balance when benefits are disbursed if the employee is entitled to more than R 3,500.

- If you are planning on topping up your employee's wage, you must confirm that the sum of the benefit and top-up amounts do not exceed the employee's normal salary.

- All of the advances need to be reflected as TERS payouts on the EMP201 for the respective month, as otherwise the employee will be subject to paying larger PAYE and UIF contributions. This is because these are calculated using balance of remuneration, which does not include TERS benefits.

Reflecting June TERS advancements correctly in EMP201s¶

If you have received TERS benefits to disburse to your employees for April and/or May, you will know the amount that each employee receives each month. These amounts should be added to each employee's payslip as a "TERS Payout", thus confirming the correct tax treatment thereof. This can be done in bulk as follows:

- Go to Employees > Bulk Actions > Payslip Inputs.

- Using the filters, select "TERS Payout" under "Other".

- Enter the amounts for each employee.

- Click Save.

Additionally, before finalising the payslip you need to also reduce the amount of employee remuneration by the value of their TERS benefit. Any sum left should reflect the amount you wish to provide as a top up. This can be done in bulk by going to Employees > Bulk Actions > Regular Inputs and reducing the wages by the corresponding amount.

Advancements already paid for April / May, but not correctly reflected in the employee's EMP201s¶

Whilst waiting for TERS benefits to be disbursed, you may have opted to pay employees a salary for April or May and also submitted an EMP201 reflecting this money as remuneration. When you then receive the benefits corresponding to a certain month, it is not correctly reflected on employee EMP201s, in order for you to recoup the money advanced.

In such a case, you should do the following:

- Download the transaction history report (Reports > Transaction History Report) and the EMP201s reflecting the PAYE and UIF liability (Go to Filing and click on PDF next to the relevant EMP201s for April / May 2020).

- Unfinalise the payslips which record the payment amount as salary (Pay Runs > Unfinalise). If these payslips are part of a pay run, you will first need to delete the pay run before you can unfinalise these payslips.

- For each employee, go to their payslip for the month in question and add the amount of TERS benefits which they are due. Additionally, reduce the amount of salary they are paid by the value of the TERS benefit they are paid. Both of these tasks can be done using the bulk inputs functionality, mentioned above.

This now reflects that:

- You have paid an advancement of TERS benefits to your employees.

-

Any amounts above and beyond the TERS benefit paid are top-up amounts which you have opted to pay your employees.

-

Finalise the amended payslips.

- Resubmit the EMP201 information to SARS using e@syFile or eFiling.

The payment of the TERS benefits to you can be used to recoup the advancement you have made.

Employee over-contributions

Your employees will have over-contributed PAYE and UIF. They will be able to recoup the excess when completing their individual tax returns, unless refunds are accommodated for in the upcoming TERS auditing process.

How do I account for TERS payouts in my books?

TERS payouts are for employees – employers are simply facilitating the process in certain instances (the UIF are largely paying TERS directly to employees as of May). Therefore, TERS payouts received are liabilities, as they are owed to employees. They will be recorded as follows:

When receiving the payout, DEBIT Bank (bank increases) and CREDIT TERS Payout Liability (liability increases). This does not get recorded on SimplePay in any way.

When paying it out to employees, DEBIT TERS Payout Liability (liability decreases) and CREDIT Bank (bank decreases). If you use integration with Xero on SimplePay, the TERS Payout system item will be mapped to a liability account in Xero.

I am not a SimplePay client, is it still possible to use your forms for UIF and TERS?

All of the forms and functionality covered on our help site are only available to SimplePay clients. The good news is that we offer a 30 day free trial and sign up is a breeze! You can find out more and sign up for a trial here. That way you can generate the relevant forms for your COVID-19 relief now and then continue to experience the joy of stress free payroll and SARS filing for years to come.

How do I get my UIF reference number?

Please contact the UIF call centre. Your request will be escalated and you will receive an email confirming your UIF number – the actual number is not given over the phone for security purposes.

I need to refund the UIF, how do I do this?

The following information has been extracted from the TERS FAQ issued by government:

Clients are advised to first email the UIF with a request for refund before making a bank transfer. Clients should email the following documents/information to [email protected], making them aware of the transfer.

- Bank statement

- UIF reference number

- Payment breakdown report

The UIF team will review the information and provide feedback as to the way forward. Should you require banking details for the transfer, please contact the call centre.

Does the type of business or the sector I'm in affect eligibility for TERS?

From the requirements given for TERS applications the type of business or sector doesn't appear to be relevant.

Employees are eligible for TERS if:

- their employer closed their operations, wholly or partially, as a result of the COVID-19 pandemic; and

- the employee contributed to UIF prior to lockdown.